Archean Chemical Industries Ltd incorporated on November 20, 2003, n is a leading specialty marine chemical manufacturer in India and focused on producing and exporting bromine, industrial salt, and sulphate of potash to customers around the world. Archean commands a leadership position in Indian bromine merchant sales by volume in Fiscal 2021. Archean exported 100% of its industrial salt production, primarily to customers in Japan and China. Archean is the largest exporter of bromine and industrial salt in India in Fiscal 2021 and has amongst the lowest cost of production globally in both bromine and industrial salt.

The company produces its products from its brine reserves in the Rann of Kutch, located on the coast of Gujarat, and manufactures products at its facility near Hajipir in Gujarat. As of June 30, 2022, they marketed their products to 18 Global customers in 13 countries and to 24 domestic customers. The company had 228 nickel and lead-lined ISO containers (owned and leased) for their export business as of June 30, 2022, required for the transportation of bromine since it is dangerous.

Promoters & Shareholding:

Chemikas Speciality LLP, Ravi Pendurthi, and Ranjit Pendurthi are the company promoters.

| Pre Issue Share Holding | 65.58% |

| Post Issue Share Holding | 53.41% |

Also read : SIP (Systematic Investment Plan) could be the key to your wealth creation

Public Issue Details:

Offer for sale: OFS of approx. 16,150,000 equity shares at Rs. 2, aggregating up to Rs. 657.31 Cr and fresh of approx. 19,778,870 equity shares at Rs. 2, aggregating up to Rs. 805 Cr.

Total IPO Size: Rs. 1,462.31 Cr.

Price band: Rs. 386 – Rs. 407.

Objective: For Redemption or earlier redemption of NCDs issued by the company and general corporate purposes.

Bid qty: minimum of 36 shares (1 lot) for Rs. 14,652 and maximum of 13 lots.

Offer period: 9th Nov 2022 – 11th Nov 2022.

Date of listing: 21st Nov 2022.

Pros:

- Leading market position, expansion, and growth in bromine and industrial salt.

- High entry barriers in the specialty marine chemicals industry.

- Established infrastructure and integrated production with cost efficiencies.

- Professional and experienced management team.

Risks:

- The inability to comply with repayment and other covenants in its financing agreements could adversely affect its business.

- Reliance on three principal products for substantially of its sales.

- Exposed to foreign currency fluctuation risks.

- No long-term agreements with suppliers.

Subscribe or avoid?

Sectorial outlook – In the calendar year 2021, the global chemicals market was valued at approximately $ 5,334 billion. The global chemicals market is expected to grow at a CAGR of 3.6% from $ 5,334 billion in the calendar year 2021 to reach $ 6,143 billion by the calendar year 2025. Rapid industrialization in India and China is expected to drive demand for specialty chemicals. Asia Pacific (APAC) dominated the global specialty chemicals market in the calendar year 2020 with a 42.0% market share, owing to its huge customer base, increasing industrial production, and robust growth of the construction sector in the region. In the calendar year 2021, the Indian chemicals industry was valued at US$178 billion, representing approximately 3-4% of the value of the global chemicals industry. The specialty chemical in India is expected to grow significantly in the coming years owing to several factors such as China+1, and various government initiatives lately, India has become an attractive destination for foreign investment owing to its large and rapidly growing consumer market in addition to a developed commercial banking network, availability of skilled manpower and a package of fiscal incentives for foreign investors. All of the above are expected to have a positive impact on the sector the company is operating in the long term.

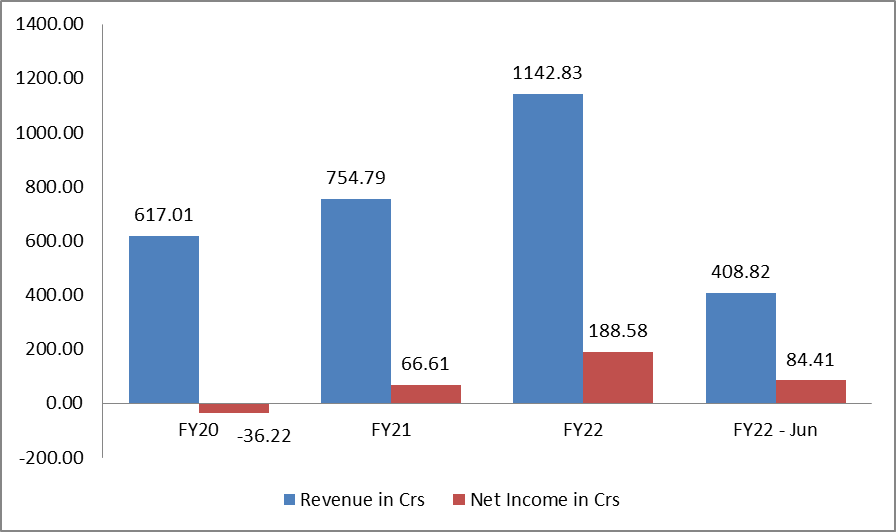

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 9.04 and the P/E is around 43x on the upper price band of Rs. 407. The EPS for FY22 is Rs. 18.2 and the P/E is around 22.2x. If we annualize Q1-FY23 EPS of Rs. 8.17, P/E is around 12x. It has Tata Chemicals Ltd (14.4x), Deepak Nitrite Ltd (31.3x), Aarti Industries Ltd (20x), and Neogen Chemicals Ltd (74x) as its listed peers as per the RHP. The company’s P/E is between 22.2x and 43x. Net margins and EPS have been growing consistently. Looking at the valuation, it seems to be reasonable.

Recommendation – The Company has a niche place as a specialty chemical manufacturer and exporter in an industry that has high entry barriers. After considering all the factors the listing still seems reasonable with good prospects hence we would recommend “Subscribe” to this IPO for investors from a medium to long-term perspective.

Disclaimer:

This article should not be construed as investment advice, please consult your Investment Adviser before making any sound investment decision.

If you do not have one visit mymoneysage.in

Also read : Debt Mutual Funds – Types, Taxation, Indexation benefit, Risk and suitability