One97 Communications Limited (“Paytm”) incorporated in December 22, 2000, is India’s leading digital ecosystem for consumers and merchants as it has built the largest payments platform in India based on the number of consumers, number of merchants, number of transactions and revenue as of March 31, 2021. The company offers its consumers a wide selection of payment options on the Paytm app, which include (i) Paytm Payment Instruments, which allow them to use digital wallets, sub-wallets, bank accounts, buy-now-pay-later, wealth management and (ii) major third-party instruments, such as debit and credit cards and net banking.

It has offered payment services, commerce and cloud services, and financial services to 337 million registered consumers and over 21.8 million registered merchants, as of June 30, 2021. The “Paytm” brand is India’s most valuable payments brand, with a brand value of $6.3 billion, and Paytm remains the easiest way to transact across multiple methods. It offer services such as Paytm Wallet, Paytm QR, Paytm Soundbox, Gold investments and Fixed Deposit, Paytm Postpaid, Merchant Cash Advance and FASTag.

Promoters & Shareholding:

‘Paytm’ is a professionally managed company with no identifiable promoters.

Public Issue Details:

Offer for sale: Fresh issue of approx. 38,604,651 equity shares of Rs. 1 aggregating up to Rs. 8,300 Cr and OFS of approx. 46,511,628 equity shares aggregating up to Rs. 10,000 Cr.

Total IPO Size: Rs. 18,300 Cr.

Price band: Rs. 2080 – Rs. 2150.

Objective: To grow and strengthen Paytm ecosystem, investing in acquisitions and for general corporate purposes.

Bid qty: minimum of 6 shares (1 lot) for Rs. 12,900 and maximum of 15 lots.

Offer period: 8th Nov 2021 – 10th Nov 2021.

Date of listing: 18th Nov 2021.

Pros:

- India’s leading digital payment service platform.

- Large customer base with 333 million total customers, 114 million annual transacting users, and 21 million registered merchants

- Professional and experienced management team.

- Strong and trusted brand identity with a brand value of $6.3 billion.

- It has deep insights about Indian merchant and consumer behaviour.

Cons:

- The company has suffered losses in the last 3 years.

- The revenue of the company has been decreasing for the last 3 years.

- It has experienced negative cash flows in the past.

- Company receives majority of the revenues from its payment services. There is increased competition from competitors i.e PhonePe, Google Pay & others.

- Paytm offers some of the services in partnership with its group company, Paytm payments Bank. In case of any failure by Paytm Payments Bank to support such services, it can have impact on business.

Also read : https://www.mymoneysage.in/blog/should-you-invest-in-sme-ipos/

Subscribe or avoid?

Sectorial outlook – The Indian digital landscape is evolving and technology is playing an important role by increasing reach and accessibility for merchants and consumers. The revolution of mobile and cloud technology, combined with growing incomes and higher consumption rates in India, is at a digital tipping point. Over the last decade, India added 500 million+ new smartphone users hence the digital payments have also been growing steadily over time. In FY 2021, digital payments market size by value stood at approximately $20 trillion with 43 billion transactions during the year and this is expected to more than double from US$ 20 trillion in FY 2021 to $40-50 trillion by FY 2026. Several factors, including government initiatives and reforms, improving technology, increasing reach and awareness is expected have positive impact on the company and its business.

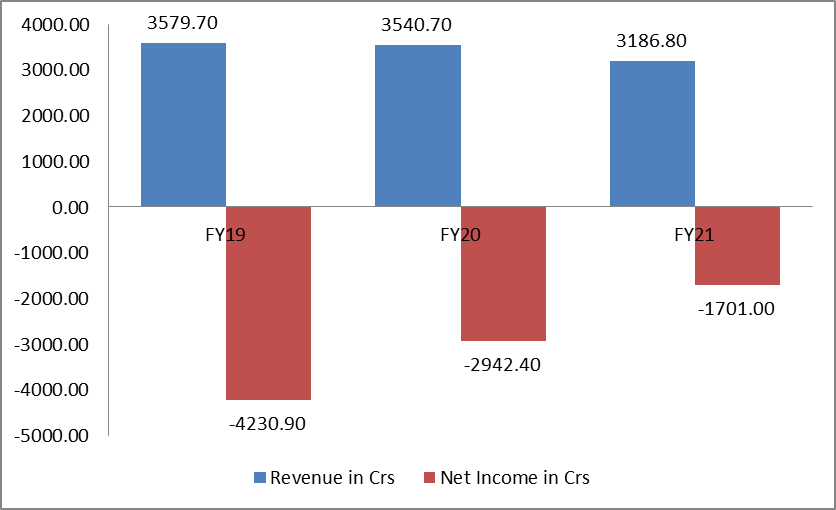

The financials (revenue and net profit) are shown in graph below:

Valuation – Since the company has suffered losses in the last 3 years, it’s not possible to determine the P/E. There are no listed peers. Even though the company is the leading player in the digital ecosystem we have to keep in mind that the company has been incurring losses and the revenue has been decreasing since the past 3 years and hence the listing seems to be very expensive. Considering the trailing twelve month (TTM) sales of Rs 3,142 crore on post issue basis, the company is going to list at a market cap/sales of 44.36 with a market cap of Rs 1,39,379 crore. If we go with the business model of the technology company, even going with the future projection, the valuation reported is on the higher side. Even if we assume 20% operating margins for platform business, PayTM has to grow at 33% CAGR over the next 10 years for IPO investors to earn a return of 13% CAGR. Apart from high valuation, the biggest bone of contention is that it is yet to deliver a profit despite being in the business for over two decades.

Recommendation – The is a massive hype around this company for being a huge player with a big market share in the digital ecosystem and considering the current bull run, huge demand for IPOs, this IPO might get oversubscribed. After considering all the factors we would recommend investors with high risk profile may “SUBSCRIBE” to this IPO for the possibility of listing gains. Investors with medium to long term perspective can skip this IPO, wait and watch the performance in future to take decision to invest.

Get your Mutual funds and Equity portfolio evaluated by a Registered Investment Advisor. It’s FREE, but spots are limited. Register now

Disclaimer:

This article should not be construed as investment advise, please consult your Investment Adviser before making any sound investment decision. If you do not have one visit mymoneysage.in now.

Also read : https://www.mymoneysage.in/blog/analysing-the-reits-in-india/