Fusion Micro Finance Limited incorporated in 1994, has a core idea of creating opportunities at the bottom of the pyramid. The company does this by providing financial services to unserved and underserved women in rural and peri-rural areas across India. The company’s responsibilities are not restricted merely to financial support, but also to acquaint the clients to manage their finances by disseminating Financial Literacy to them. It is one of the youngest companies (in terms of getting an NBFC-MFI license) among the top NBFC-MFIs in India in terms of AUM as of June 30, 2022. The company’s business runs on a joint liability group-lending model, wherein a small number of women form a group (typically comprising five to seven members) and guarantee one another’s loans.

The company has achieved a significant footprint across India, where it has extended its reach to 2.90 million active borrowers who were served through its network of 966 branches and 9,262 permanent employees spread across 377 districts in 19 states and union territories in India, as of June 30, 2022.

Promoters & Shareholding:

Devesh Sachdev, Creation Investments Fusion, LLC, Creation Investments Fusion II, LLC, and Honey Rose Investment Ltd are the company’s promoters.

Also read : Do you have your Retirement plan in place?

Public Issue Details:

Offer for sale: OFS of approx. 13,695,466 equity shares at Rs. 10, aggregating up to Rs. 503.99 Cr and fresh of approx. 16,304,347 equity shares at Rs. 10, aggregating up to Rs. 600 Cr.

Total IPO Size: Rs. 1,103.99 Cr.

Price band: Rs. 350 – Rs. 368.

Objective: To augment the capital base of the company.

Bid qty: minimum of 40 shares (1 lot) for Rs. 14,720 and maximum of 13 lots.

Offer period: 2nd Nov 2022 – 4th Nov 2022.

Date of listing: 15th Nov 2022.

Pros:

- A long history of serving rural markets with high growth potential in the microfinance segment.

- Well Diversified and Extensive Pan-India Presence with no single state contributing more than 20% of its total AUM.

- Access to Diversified Sources of Capital and Effective Asset Liability Management.

- Stable and Experienced Management Team Supported by Marquee Investors.

Risks:

- An increase in the level of our NPAs or provisions may adversely affect its business.

- Certain provisions of the NBFC-ND-SI Master Directions and the RBI (RFML) Directions impose requirements that restrict its business.

- Any downgrade of its credit ratings may constrain access to capital.

Subscribe or avoid?

Sectorial outlook – The microfinance industry (Joint-liability group (“JLG”) portfolio) has recorded healthy growth in the past few years. The industry’s gross loan portfolio (“GLP”) increased at a CAGR of 21% since the financial year 2018 to reach approximately Rs. 3.1 trillion in the first quarter of the financial year 2023. The growth rate for NBFC-MFIs is the fastest as compared to other player groups. MFI Industry to grow at 18-20% CAGR between FY2022-2025. During the same period, NBFC-MFIs are expected to grow at a much faster rate of 20-22% as compared to the MFI industry. Key drivers behind the superior growth outlook of the MFI industry include increasing penetration into the hinterland and expansion into newer states, faster growth in the rural segment, expansion in average ticket size, and support systems like credit bureaus. The presence of self-regulatory organizations (SRO) like MFIN and Sa-Dhan is also expected to support the sustainable growth of the industry going forward. The microfinance sector in India is regulated by the RBI and The RBI’s new regulatory regime for microfinance loans effective April 2022 has done away with the interest rate cap applicable on loans given by NBFC-MFIs, and also supports growth by enabling players to calibrate pricing in line with customer risk. All of the above are expected to positively impact the sector the company is operating in the long term.

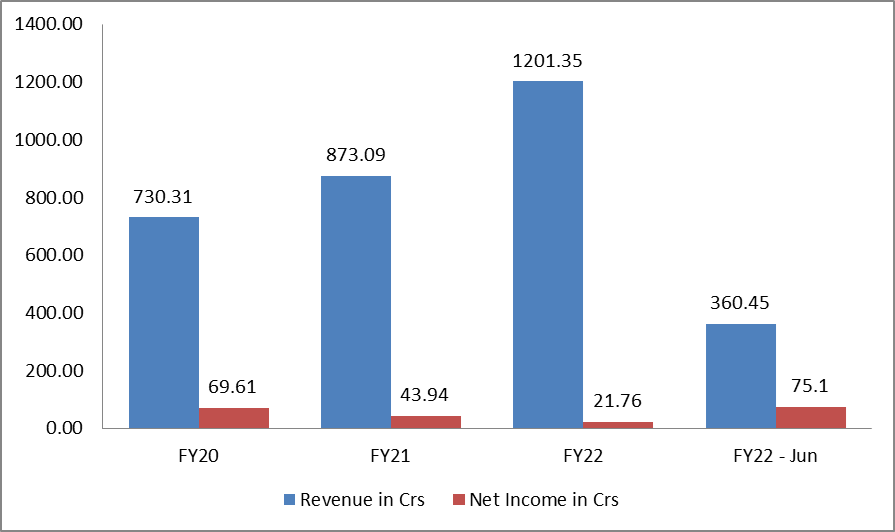

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 6.22 and the P/E is around 59x on the upper price band of Rs. 368. The EPS for FY22 is Rs. 2.67 and the P/E is around 137.8x. If we annualize Q1-FY23 EPS of Rs. 9, P/E is around 11x. It has Ujjivan Small Finance Bank (225x), CreditAccess Grameen (26.5x), Spandana Sphoorty (17.2x), and Suryoday bank as its listed peers as per the RHP. The company’s P/E is between 11x and 59x. The company’s revenue has been growing consistently but the margin in the last few years have been dipping. Looking at the valuation, it appears to be a little expensive.

Recommendation – The rural economy is far more resilient today due to two consecutive years of good monsoons, increased spending under MNREGA and irrigation programmes, etc. Rural India Accounts for about half of the GDP, but only about 9% of Total Credit and 11% of Total Deposits hence it remains extremely under penetrated currently and the company is attempting to fill this void. After considering all the factors the listing still seems reasonable with good prospects but there are some issues regarding margin hence we would recommend “Subscribe” to this IPO for investors with a high-risk appetite from a medium to long-term perspective.

Disclaimer:

This article should not be construed as investment advice, please consult your Investment Adviser before making any sound investment decision.

If you do not have one visit mymoneysage.in

Also read : Debt Mutual Funds – Types, Taxation, Indexation benefit, Risk and suitability