Tata Technologies Ltd stands at the forefront of global engineering services, renowned for its comprehensive offerings in product development and digital solutions. Established on August 22, 1994, and promoted by Tata Motors Ltd, the company has evolved into a powerhouse in the industry, delivering turnkey solutions to global Original Equipment Manufacturers (OEMs) and their Tier-1 suppliers.

With a focal point on manufacturing-led verticals, Tata Technologies excels in automotive solutions, constituting a substantial 75% of its revenue. Beyond automotive, the company extends its expertise to aerospace and transportation and construction heavy machinery (TCHM). Proficient in both product engineering and manufacturing engineering within the mechanical domain, Tata Technologies is progressively broadening its capabilities in software and embedded engineering.

As a pure-play manufacturing-focused Engineering Research & Development (ER&D) company, Tata Technologies holds a pivotal position in the automotive sector. In 2022, the company engaged with 7 of the Top-10 automotive ER&D spenders and 5 of the 10 prominent new energy ER&D spenders, a testament to its industry leadership.

Distinguished by a diversified global client base, Tata Technologies operates through 19 global delivery centers strategically located across North America, Europe, and the Asia Pacific. The company’s commitment to excellence is further underscored by robust partnerships and alliances with industry leaders such as Dassault, Logility, Siemens Industry Software Inc., Codincity, Fantasy, and leveraging Microsoft AZURE products/services. These collaborations enhance Tata Technologies’ capabilities, enabling the expansion of its client reach across various verticals and geographies.

A significant milestone in the company’s growth trajectory is its recent empanelment by Airbus, which is anticipated to emerge as a potent avenue for future growth. Tata Technologies continues to be at the forefront of innovation, shaping the landscape of engineering services on a global scale.

Promoters & Shareholding:

Tata Motors Limited is the Promoter of the company.

| Particulars | Pre – Issue | Post – Issue |

| Promoters – Tata Motors Ltd | 64.79% | 53.39% |

| Promoter Group | 2.00% | 2.00% |

| Public – Investors Selling S/h | 10.89% | 7.29% |

| Public – Others | 22.32% | 37.32% |

Public Issue Details:

Offer for sale: OFS of approx. 60,850,278 equity shares at Rs. 2, aggregating up to Rs. 3,042.51 Cr.

Total IPO Size: Rs. 3,042.51 Cr.

Price band: Rs. 475 – Rs. 500.

Objective: To carry out OFS by the Selling Shareholders and to gain benefits of listing on a stock exchange.

Bid qty: minimum of 30 shares (1 lot) for Rs. 15,000 and maximum of 13 lots.

Offer period: November 22, 2023 – November 24, 2023.

Date of listing: December 5, 2023.

Pros:

- The company provides end-to-end automotive ER&D services, from concept design to launch.

- Distinctive expertise in emerging automotive trends, including electric vehicles (EVs), connectivity, and autonomous technologies.

- The company’s digital services and accelerators aid OEMs and Tier-1 suppliers in managing the entire product life cycle and engaging customers.

- The company maintains a global presence in Asia Pacific, Europe, and North America, partnering with major manufacturing enterprises worldwide.

- Global delivery model enabling intimate client engagement and scalability.

Risks:

- The company heavily relies on its promoter and a few key clients for a substantial portion of its revenues, with Tata Motors (Promoter), its subsidiaries, and JLR being among the top five clients by revenue in Fiscal 2022.

- The company’s revenues are significantly dependent on clients within the automotive segment. Therefore, an economic slowdown or any adverse factors impacting this sector may negatively affect the business.

- The company has experienced negative cash flows in the past and may continue to face similar challenges in the future.

Subscribe or avoid?

Sectorial outlook – ER&D services, comprising product and process engineering, play a pivotal role in designing, developing, and maintaining products and processes for sale. In 2022, the global ER&D spend reached an estimated USD 1.8 trillion, with USD 810 billion attributed to digital engineering. Despite macro headwinds, including geopolitical uncertainties and inflation, the industry is expected to remain resilient, with a steady growth trajectory.

The digital engineering spend, focusing on technologies like IoT, blockchain, 5G, AR/VR, cloud engineering, digital thread initiatives, advanced analytics, embedded engineering, and AI/ML, is projected to post a robust CAGR of ~16% from CY22 to CY26. The global ER&D spend is highly consolidated, with the top 1000 enterprises accounting for ~85% of the market. Manufacturing-led verticals, particularly automotive, contribute significantly, comprising almost half of the global ER&D spending.

The software and internet sector, the largest ER&D vertical, is expected to continue its rapid growth, accounting for ~20% of the global spend. Services-led verticals, primarily driven by digital engineering investments, are the fastest-growing category, representing ~12% of the global ER&D spend.

In terms of geography, North America leads in global ER&D spend, with a focus on software and internet firms. The APAC region, driven by increased spending from Southeast Asian enterprises and high digital engineering expenditures by hi-tech firms, is anticipated to surpass Western Europe. China, contributing over a tenth of global ER&D spending, particularly in automotive, semiconductor, and software and internet, is a key player in the industry, with a strong emphasis on battery EVs.

As the industry evolves towards digital transformation and emerging technologies, Tata Technologies is well-positioned. With its focus on manufacturing-led verticals, including automotive, and a diversified global presence, Tata Technologies is poised to capitalize on the growing demand for digital engineering solutions. The company’s expertise in ER&D services aligns with industry trends, offering innovative solutions to OEMs and Tier-1 suppliers. As the sector advances, Tata Technologies is expected to play a crucial role in shaping the future of engineering services.

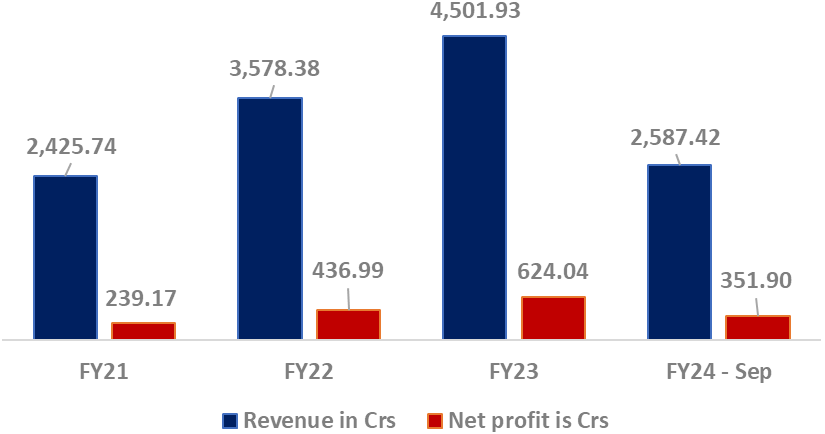

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 10.68 and the P/E is around 46.8x on the upper price band of Rs. 500. The EPS for FY23 is Rs. 15.38 and the P/E is around 32.5x. If we annualize Q2-FY23 EPS of Rs. 17.34, P/E is around 28.8x. It has KPIT Techno (134.34x), L & T Technologies (39.45x), and Tata Elxsi (67.06x) as their listed peers as its listed peers as per the RHP. The company’s P/E is between 28.8x and 46.8x. ROA is around 13.6%, ROE and ROCE are currently 24.6% and 22.73% respectively. Revenue has been growing consistently and the margins have also been consistently increasing.

Recommendation

This portion will be available to our clients only.