Landmark Cars Limited incorporated on February 23, 2006, is a leading premium automotive retail business in India with dealerships for Mercedes-Benz, Honda, Jeep, Volkswagen, and Renault. They also cater to the commercial vehicle retail business of Ashok Leyland in India. It offers services such as sales of new vehicles, after-sales service, and repairs (including sales of spare parts, lubricants, and accessories), sales of pre-owned passenger vehicles, and facilitation of the sales of third-party finance and insurance products. It operates on 2 business models: i) facilitate the sale of used vehicles through its appointed panel of agents on a commission basis and ii) Take the vehicles on their books for sale after any needed refurbishment.

The company operates as an authorized service center for Mercedes-Benz, Honda, Volkswagen, Jeep, Renault, and Ashok Leyland. Landmark Cars also provide after-sales service and repairs through 51 after-sales services and spare outlets, as of September 30, 2021. Its vehicle dealership network is spread across 31 cities in eight states and union territories including Maharashtra, Uttar Pradesh, Gujarat, Haryana, Madhya Pradesh, Punjab, West Bengal, and the National Capital Territory of Delhi.

Promoters & Shareholding:

Sanjay Karsandas Thakker is the company promoter.

Also Read: Should You benchmark your investment Portfolio?

Public Issue Details:

Offer for sale: OFS of approx. 2,964,427 equity shares at Rs. 5, aggregating up to Rs. 150 Cr and fresh of approx. 7,944,664 equity shares at Rs. 5, aggregating up to Rs. 402 Cr.

Total IPO Size: Rs. 552 Cr.

Price band: Rs. 481 – Rs. 506.

Objective: For repayment/ prepayment of certain borrowings and general corporate purposes.

Bid qty: minimum of 29 shares (1 lot) for Rs. 14,674 and maximum of 13 lots.

Offer period: 13th Dec 2022 – 15th Dec 2022.

Date of listing: 23rd Dec 2022.

Pros:

- Leading automotive dealership for major OEMs with a strong focus on high-growth segments.

- Growing presence in the after-sales segment.

- Comprehensive business model.

- Professional and experienced management team.

Risks:

- The company is subject to the influence of, and restrictions imposed by OEMs under the terms of the dealership or agency agreements.

- Dependent on the OEM.

- The company has reported a loss in fiscal 2020 and 2019 and may incur additional losses in the future.

Subscribe or avoid?

Sectorial outlook – In the last five years, the premium vehicles segment has grown at a healthy 8.1% CAGR, expanding its contribution from 42% in Fiscal 2017 to 63% in Fiscal 2022. On the other hand, mass-market vehicle sales contracted at a CAGR of 9%, with its market share decreasing from 58% in Fiscal 2017 to 37% in Fiscal 2022. The Indian PV (mass and premium segments) industry as a whole, in terms of sales volume, grew by a CAGR of 5.3% between Fiscal 2017 and Fiscal 2019, primarily due to an increase in demand driven by improved economics, higher affordability, and launches of new automobile modes. The industry, in terms of sales volume, contracted in Fiscal 2020 and Fiscal 2021, mainly due to mandatory implementation of BSVI norms, national lockdown, economic uncertainty, and struggling vehicle supply. As the COVID-19 pandemic eases and economic sentiment improved, the sales volume of the Indian PV (mass and premium segment) industry increased by a year-on growth of 13% in Fiscal 2022. Going forward, The overall PV sales, in terms of sales volume, are expected to grow at a CAGR of 8 to 10% from approximately 3.1 million units in Fiscal 2022 to approximately 4.6-4.8 million units in Fiscal 2027. All of the above are expected to have a positive impact on the sector the company is operating in the long term.

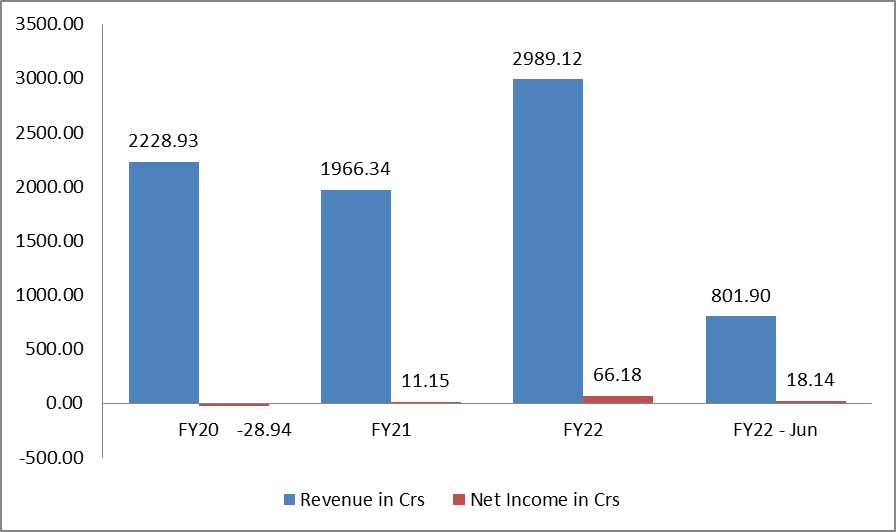

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 4.3 and the P/E is around 115x on the upper price band of Rs. 506. The EPS for FY22 is Rs. 17.8 and the P/E is around 28x. If we annualize Q1-FY23 EPS of Rs. 4.8, P/E is around 26x. It has no listed peers as per the RHP. The company’s P/E is between 115x and 26x. It has been able to maintain its net margins in the last few quarters and EPS has also been growing consistently. Looking at the valuation, it seems to be reasonable.

Recommendation – The Company is a leading automotive dealership for major OEMs with a high market share in the premium automotive retail segment and it also provides comprehensive after-sales service on vehicles. However not to forget it operates in a very competitive market. After considering all the factors the listing seems good for investors with a long term horizon to “Subscribe” to this IPO. Buy on dips could be another strategy as well.

Disclaimer:

This article should not be construed as investment advice, please consult your Investment Adviser before making any investment decision.

If you do not have one visit mymoneysage.in

Also Read: Market Outlook Dec’22