Bikaji Foods International Limited incorporated on October 6, 1995, is the 3rd largest ethnic snacks company in India with an international footprint and 2nd fastest growing company in the Indian organized snacks market. They were the largest manufacturer of Bikaneri bhujia with an annual production of 29,380 tonnes, and they were the 2nd largest manufacturer of handmade papad with an annual production capacity of 9,000 tonnes in Fiscal 2022. They are also the 3rd largest player in the organized sweets market with an annual capacity of 24,000 tonnes for packaged rasgulla, 23,040 tonnes for soan papdi, and 12,000 tonnes for gulab jamun.

The company’s product range includes six principal categories: bhujia, namkeen, packaged sweets, papad, western snacks as well as other snacks which primarily include gift packs (assortment), frozen food, mathri range, and cookies. In the six months that ended June 30, 2022, the company sold more than 300 products under the Bikaji brand. It has developed a large pan-India distribution network. As of June 30, 2022, they had 6 depots, 38 super-stockists, 416 direct, and 1,956 indirect distributors that work with their super-stockists. The company has 7 manufacturing facilities that are operated by them, with 4 facilities located in Bikaner, 1 in Guwahati, 1 in Tumakuru, and 1 in Muzaffarpur. It has also exported its products to 21 international countries, including countries in North America, Europe, the Middle East, Africa, and Asia Pacific.

Promoters & Shareholding:

Shiv Ratan Agarwal, Deepak Agarwal, Shiv Ratan Agarwal (HUF), and Deepak Agarwal (HUF) are the company promoters.

Also Read: Floating Rate Bond Vs NSC

Public Issue Details:

Offer for sale: OFS of approx. 29,373,984 equity shares at Rs. 1, aggregating up to Rs. 881.22 Cr.

Total IPO Size: Rs. 881.22 Cr.

Price band: Rs. 285 – Rs. 300.

Objective: To achieve the benefits of listing equity shares on the Stock Exchanges.

Bid qty: minimum of 50 shares (1 lot) for Rs. 15,000 and maximum of 13 lots.

Offer period: 3rd Nov 2022 – 7th Nov 2022.

Date of listing: 16th Nov 2022.

Pros:

- Diversified product portfolio focused on various consumer segments and markets.

- 3rd largest player in the organized sweets market.

- A well-established brand with pan-India recognition.

- The company has strategically-located large-scale sophisticated manufacturing facilities with stringent quality standards.

- Professional and experienced management team.

Risks:

- The business is manpower intensive and may be adversely affected by work stoppages, increased wage demands by employees, or an increase in minimum wages across various states.

- Subject to various contamination-related risks which typically affect the FMCG industry.

- The company has made investments in debt instruments that are not secured.

- Any material fluctuation in foreign currency exchange rates may impact its results of operations since it does not have a formal hedging policy.

Subscribe or avoid?

Sectorial Outlook – India’s packaged food business is currently valued at Rs. 4,240 billion. It has grown significantly in the last five years on account of changing lifestyles, rising incomes, and urbanization. In Fiscal 2015, the packaged food retail revenue was worth Rs. 2,434 billion and registered a CAGR of approximately 8.3% from Fiscal 2015 to Fiscal 2022. It is estimated to grow at a CAGR of 8% in the next five years to reach Rs. 5,798 billion. Indian Savoury Snacks market is valued at Rs. 751 billion in 2022 and is expected to reach Rs. 1,227 billion by 2026 at a CAGR of 13%. Indian savory and snacks market is characterized by a large number of unorganized players across the product segments however; the organized segment has been strengthening its position in the market over the last few years, with new product launches and product innovations that have been largely targeted at the urban as well as the rural consumer. The popularity of traditional sweets coupled with increasing consumer awareness of cleanliness and hygiene has assured that packaged sweets have acquired a good amount of traction.

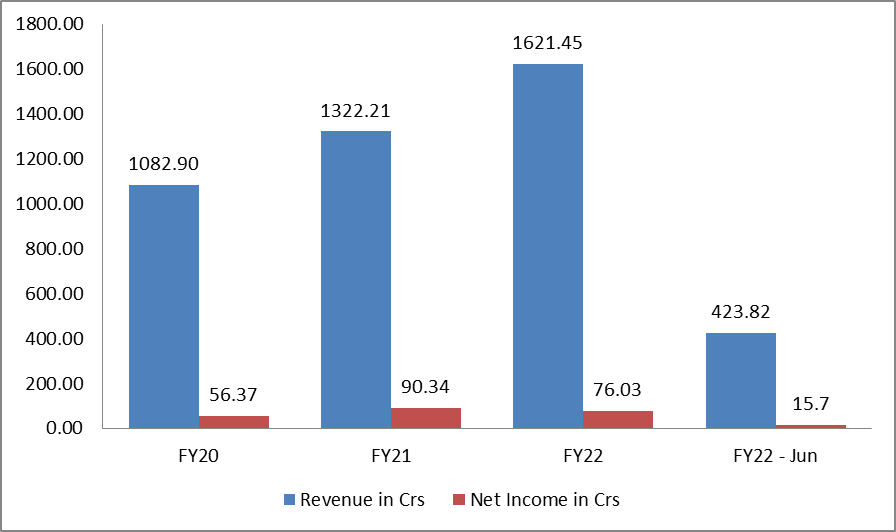

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 3.06, and the P/E is around 98x on the upper price band of Rs. 300. The EPS for FY22 is Rs. 3.15 and the P/E is around 95x. If we annualize Q1-FY23 EPS of Rs. 0.65, P/E is around 115x. It has Prataap Snacks (305x), DFM Foods, Nestle India (83.6x), and Britannia (61.4x) as its listed peers as per the RHP. The company’s P/E is between 95x and 98x. Its revenue has been growing consistently but the margins have been dipping. Looking at the valuation, it seems to be expensive when compared to its peers.

Recommendation – The Company is one of India’s largest FMCG brands, it has a diversified product portfolio that has a pan-India recognition and it has been able to maintain consistent revenue growth but whether it will be able to maintain margins moving forward is the main question. After considering all the factors the listing seems aggressively priced hence we would recommend only investors with surplus cash and a high-risk appetite to “Subscribe” to this IPO medium to long-term perspective.

Disclaimer:

This article should not be construed as investment advice, please consult your Investment Adviser before making any sound investment decision.

If you do not have one visit mymoneysage.in

Also read : Debt Mutual Funds – Types, Taxation, Indexation benefit, Risk and suitability