Five Star Business Finance Ltd incorporated in 1984, is an NBFC-ND-SI providing secured business loans to micro-entrepreneurs and self-employed individuals, each of whom are largely excluded by traditional financing institutions. It is headquartered in Chennai, Tamil Nadu with a strong presence in south India, and all of our loans are secured by our borrowers’ property, predominantly SORP. It has more than Rs. 3000 Crs in Gross Term Loans and it also has the fastest Gross Term Loans growth, with a CAGR of 65% in the last 3 years.

The company had an extensive network of 311 branches as of June 30, 2022, spread across approximately 150 districts, 8 states, and 1 union territory, with Tamil Nadu, Andhra Pradesh, Telangana, and Karnataka being their key states. They are backed by marquee institutional investors such as TPG Capital, Sequoia Capital, Matrix Partners, Norwest Venture Partners, KKR, and TVS Capital Funds Ltd.

Promoters & Shareholding:

Lakshmipathy Deenadayalan, Hema Lakshmipathy, Shritha Lakshmipathy, Matrix Partners India Investment Holdings II, LLC, and SCI Investments V are the company promoters.

Also read : Debt Mutual Funds – Types, Taxation, Indexation benefit, Risk and suitability

Public Issue Details:

Offer for sale: OFS of approx. 41,351,266 equity shares at Rs. 1, aggregating up to Rs. 1,960.01 Cr.

Total IPO Size: Rs. 1,960.01 Cr.

Price band: Rs. 450 – Rs. 474.

Objective: To get benefits from listing in the stock exchanges.

Bid qty: minimum of 31 shares (1 lot) for Rs. 14,694 and maximum of 13 lots.

Offer period: 9th Nov 2022 – 11th Nov 2022.

Date of listing: 21st Nov 2022.

Pros:

- Fastest Gross Term Loans growth among the compared peers.

- Strong “on-ground” collections infrastructure leading to the ability to maintain robust asset quality.

- 100% in-house sourcing, a comprehensive credit assessment, and robust risk management and collections framework, leading to good asset quality.

- Professional and experienced management team.

Risks:

- Any downgrade in the credit ratings could increase the borrowing costs.

- Persistently high inflation levels have hurt its business sentiments.

- Non-compliance with the RBI’s observations made pursuant to its periodic inspections could expose it to certain penalties and restrictions.

Subscribe or avoid?

Sectorial outlook – The microfinance industry has recorded healthy growth in the past few years. The industry’s gross loan portfolio increased at a CAGR of 21% since the financial year 2018 to reach approximately Rs. 3.1 trillion in the first quarter of the financial year 2023. The growth rate for NBFC-MFIs is the fastest as compared to other player groups. MFI Industry to grow at 18-20% CAGR between FY2022-2025. During the same period, NBFC-MFIs are expected to grow at a much faster rate of 20-22% as compared to the MFI industry. Key drivers behind the superior growth outlook of the MFI industry include increasing penetration into the hinterland and expansion into newer states, faster growth in the rural segment, expansion in average ticket size, and support systems like credit bureaus. The presence of self-regulatory organizations (SRO) like MFIN and Sa-Dhan is also expected to support the sustainable growth of the industry going forward. The microfinance sector in India is regulated by the RBI and The RBI’s new regulatory regime for microfinance loans effective April 2022 has done away with the interest rate cap applicable on loans given by NBFC-MFIs, and also supports growth by enabling players to calibrate pricing in line with customer risk. All of the above are expected to positively impact the sector the company is operating in the long term.

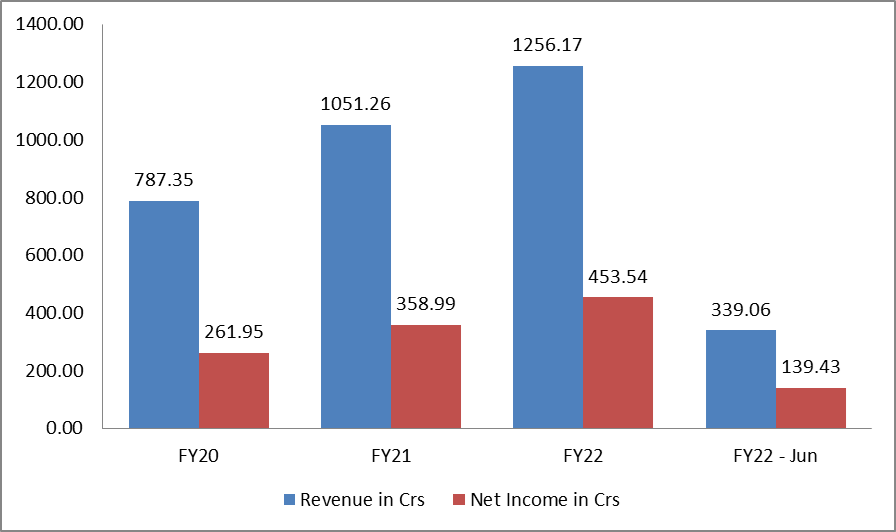

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 413.2 and the P/E is around 36x on the upper price band of Rs. 474. The EPS for FY22 is Rs. 15.92 and the P/E is around 29.77 x. If we annualize Q1-FY23 EPS of Rs. 4.74, P/E is around 25x. It has AAVAS Financiers Ltd (37.5x), Aptus Value Housing Finance (38.8x), and AU Small Finance Bank (32.6x) as its listed peers as per the RHP. The company’s P/E is between 22.5x and 42x. Net margins and EPS have been growing consistently. Looking at the valuation, it seems to be reasonable.

Recommendation – Five Star Business has witnessed robust and steady growth in its loan portfolio for the last four years and it has created a business model based on identifying an appropriate risk framework and the ideal installment-to-income ratio to make sure that customers have the resources to repay the loan after meeting their regular obligations and this has helped the firm grow its margins consistently but in the current high-interest rate environment, whether it would be able to maintain its margins will be the question. After considering all the factors the listing still seems reasonable with good prospects hence we would recommend “Subscribe” to this IPO for investors from a medium to long-term perspective.

Disclaimer:

This article should not be construed as investment advice, please consult your Investment Adviser before making any sound investment decision.

If you do not have one visit mymoneysage.in