Medplus Health Services Limited incorporated on November 30, 2006, is India’s second-largest pharmacy retailer in terms of the number of stores and revenue. The company offers a wide range of products, including i) pharmaceutical and wellness products, including medicines, vitamins, medical devices, and test kits, and ii) fast-moving consumer goods, such as home and personal care products, including toiletries, baby care products, soaps and detergents, and sanitizers. It is also the first pharmacy retailer in India to offer an omnichannel platform wherein customers can purchase products through stores, place orders over the telephone, online orders, and a Click and Pick facility.

Get your Free Wealth Management Tool, to explore your path to Financial Freedom now!

The number of company stores has grown since the conception of its business and, as of September 30, 2021, it operated 546 stores in Karnataka, 475 stores in Tamil Nadu, 474 stores in Telangana, 297 stores in Andhra Pradesh, 224 stores in West Bengal, 221 stores in Maharashtra and 89 stores in Odisha.

Promoters & Shareholding:

Gangadi Madhukar Reddy, Lone Furrow Investments Pvt Ltd, and Agilemed Investments Pvt Ltd are the company promoters.

| Pre Issue Share Holding | 43.16% |

| Post Issue Share Holding | 40.43% |

Public Issue Details:

Offer for sale: Fresh issue of approx. 7,537,688 equity shares at Rs. 2, aggregating up to Rs. 600 Cr and OFS of approx. 10,028,894 equity shares, aggregating up to Rs. 798.30 Cr.

Total IPO Size: Rs. 1,398.30 Cr.

Price band: Rs. 780 – Rs. 796.

Objective: For funding working capital requirement of subsidiary (Optival) and for general corporate purpose.

Bid qty: minimum of 30 shares (1 lot) for Rs. 15,000 and maximum of 13 lots.

Offer period: 13th Dec 2021 – 15th Dec 2021.

Date of listing: 23rd Dec 2021.

Also read : All you need to know about RBI’s Retail Direct Scheme

Pros:

- India’s second-largest pharmacy retailer in terms of the number of stores and revenue.

- Established brand and value proposition to customers.

- Professional and experienced management team.

- First pharmacy retailer to provide Omni-channel platform to customers.

- The Omni-channel proposition allows them to deepen and extend their customer reach.

Cons:

- There have been instances of negative cash flows in the last three financial years.

- Changes in prescription drug pricing and commercial terms could adversely affect its operations.

- The company is subject to regulatory scrutiny and any non-compliance will affect the company’s business.

- Disruptions in its product supply chain could adversely impact.

Subscribe or avoid?

Sectorial outlook – India’s domestic pharmaceutical market was valued at Rs. 1,500 billion in the financial year 2020, having grown at a CAGR of approximately 10% in the last five years and is expected to grow at a similar rate going forward. As of the financial year 2020, the pharmacy retail industry was estimated to be worth approximately Rs. 1,725 billion, and expected to grow at a CAGR of approximately 10% in the next five years. Whilst the per capita health expenditure in India is one of the lowest in the world, with total health expenditure comprising 3.5% of India’s GDP (compared to the global average of 6.5%), there is a high potential for growth given an increasing awareness, affordability, and acceptability of health services leading to increased spending on healthcare.

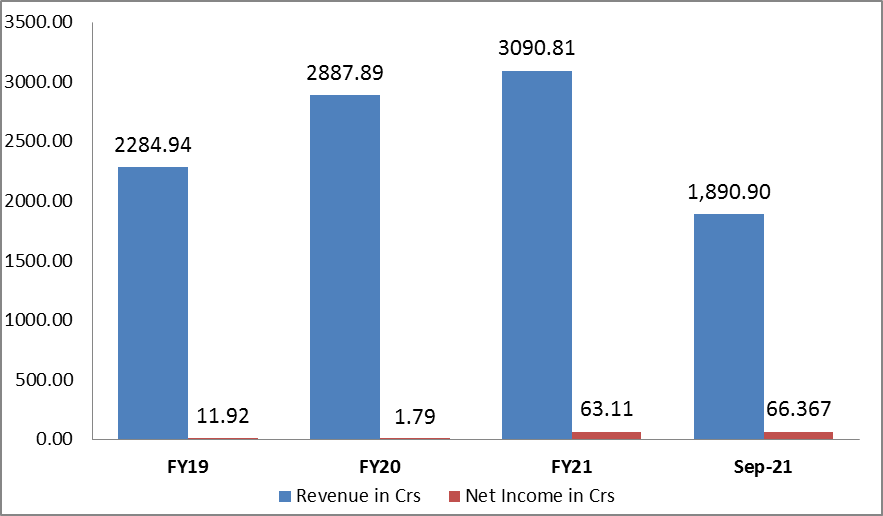

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 3.19 and the P/E is around 250x on the upper price band of Rs. 796. The EPS for FY21 is Rs. 5.88 and the P/E is around 135x. If we look at the first 6 months ended at Sep-21 and annualize it to FY22 then the EPS is Rs. 6.16 and the P/E is around 129x. The company has no listed peers as per the RHP. The company P/E is between 250x and 129x and after considering all the factors, the listing seems to be expensive.

Recommendation – The Company is the 2nd largest pharmacy retailer in India and the revenues and as well as profit margin has been increasing but the listing seems to be very expensive and whether it would be able to continue the growth in the future is a big question. However the GMP seems to be around 40% which makes a case for listing gains. After considering all the factors we would recommend investors with high-risk appetite to “SUBSCRIBE” whereas moderate and conservative investors can “AVOID” this IPO.

Disclaimer:

This article should not be construed as investment advise, please consult your Investment Adviser before making any sound investment decision. If you do not have one visit mymoneysage.in

Also read : Market Outlook – Dec’21