Rategain Travel Technologies Limited incorporated in 2004, is one of the leading distribution technology companies globally and the largest Software as a Service (SaaS) provider in the travel and hospitality industry in India. It offers travel and hospitality solutions across a wide spectrum of verticals including hotels, airlines, online travel agents (“OTAs”), meta-search companies, vacation rentals, package providers, car rentals, rail, travel management companies, cruises and ferries.

Get your Free Wealth Management Tool, to explore your path to Financial Freedom now!

Rategain Travel delivers travel and hospitality technology solutions through the SaaS platform through 3 business units; i) Data as a Service (DaaS), ii) Distribution, and iii) Marketing Technology (MarTech). The company serves 1,462 customers including eight Global Fortune 500 companies and its customers include Six Continents Hotels, Inc., an InterContinental Hotels Group Company, Kessler Collection, Lemon Tree Hotels Limited and Oyo Hotels and Homes Private Limited. It serves its customers in multiple geographies with local go-to market teams and as of September 30, 2021, have offices in six countries.

Promoters & Shareholding:

Bhanu Chopra and Megha Chopra are the company promoters.

| Pre Issue Share Holding | 67.29% |

| Post Issue Share Holding |

Public Issue Details:

Offer for sale: Fresh issue of approx. 8,823,529 equity shares of Rs. 1 aggregating up to Rs. 375 Cr and OFS of approx. 22,605,530 equity shares aggregating up to Rs. 960.74 Cr.

Total IPO Size: Rs. 1,335.74 Cr.

Price band: Rs. 405 – Rs. 425.

Objective: For repayment and/or prepayment of indebtedness availed by Rategain UK, strategic investments, acquisition, and inorganic growth and to purchase capital equipment for the company’s data centre.

Bid qty: minimum of 35 shares (1 lot) for Rs. 14,875 and maximum of 13 lots.

Offer period: 7th Dec 2021 – 9th Dec 2021.

Date of listing: 17th Dec 2021.

Also read : Should you invest in DSP Nifty 50 equal-weight ETF?

Pros:

- One of the leading distribution technology companies globally and the largest Software as a Service (SaaS) provider in the travel and hospitality industry in India.

- Marquee global customers with long-term relationships.

- Professional and experienced management team.

- It offers a comprehensive platform of industry-specific solutions with growth and monetization capabilities.

- Diverse and comprehensive portfolio of revenue maximization and business critical solutions.

Cons:

- COVID-19 pandemic has had and still might have a significant adverse effect on our business and operations.

- Required to comply with certain restrictive covenants under their financing agreement.

- May be subject to certain liability as part of its contracts with customers.

- Exposed to exchange rate risks.

Subscribe or avoid?

Sectorial outlook – Third party travel and hospitality technology is estimated to be a $ 5.91 billion market in 2021 growing to an estimated $ 11.47 billion in 2025 at a CAGR of 18%. Enterprise applications focused on guest acquisition, distribution, revenue maximization and wallet share expansion in the hospitality and travel industry have a serviceable addressable market size of $4.34 billion in 2021, growing to an estimated US$ 8.45 billion in 2025. This is a large and rapidly growing addressable market opportunity for a vertical specific platform company like Rategain. The travel technology segment is further favored by industry tailwinds of digitization in the post COVID times and this are expected to have positive impact on the company and its business.

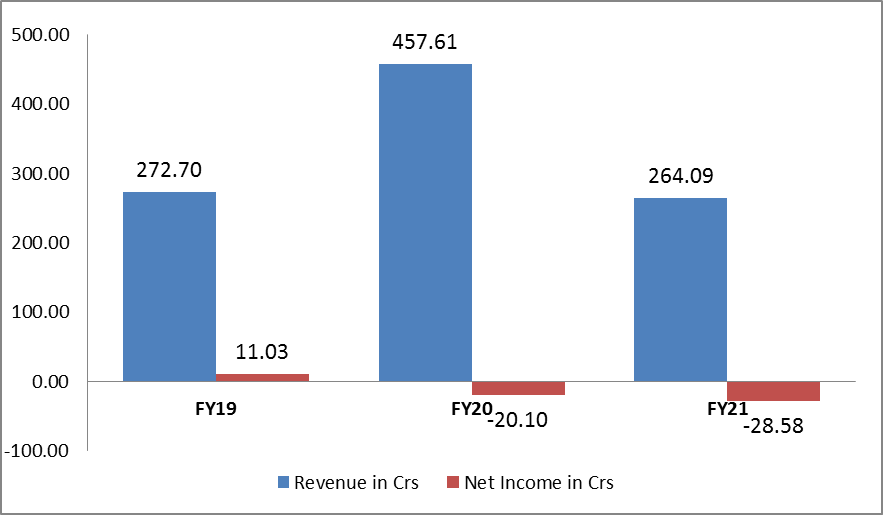

The financials (revenue and net profit) are shown in the graph below:

Valuation – In the last 3 years and also in FY21, the company has incurred losses (which is mainly due to acquisitions, as per the company’s management) hence the P/E is cannot be calculated. There are no listed peers as per the company. Since we cannot determine the P/E, it’s also not possible to determine whether the listing is reasonable or not.

Recommendation – The hospitality industry has been massively affected by the pandemic and now the new variant also threatens the sector but the company has been able to diversify its product portfolio and been able to improve its margin a bit. If you consider the GMP as on 3rd Dec is Rs.140 which is indicating listing gains.

After considering all the factors we would recommend investors with cash surplus and high risk appetite to subscribe to this IPO from a long term perspective but conservative investors can skip this IPO.

Also read : All you need to know about RBI’s Retail Direct Scheme

Disclaimer:

This article should not be construed as investment advise, please consult your Investment Adviser before making any sound investment decision. If you do not have one visit mymoneysage.in now.