Adani Wilmar Limited incorporated on 22nd January 1999, is a joint venture between Adani Group and the Wilmar Group. It is one of the few large FMCG food companies in India to offer most of the essential kitchen commodities for Indian consumers, including edible oil, wheat flour, rice, pulses, and sugar. The company’s portfolio of products spans 3 categories; i) edible oil, ii) packaged food and FMCG, and iii) industry essentials. The company also offers a diverse range of industry essentials, including oleo chemicals, castor oil and its derivatives, and de-oiled cakes.

Get your Free Wealth Management Tool, to explore your path to Financial Freedom now!

“Fortune”, the company’s flagship brand, is the largest selling edible oil brand in India. The company has strong raw material sourcing capabilities and was India’s largest importer of crude edible oil as of March 31, 2021. It has 22 plants that are strategically located across 10 states in India, comprising 10 crushing units and 19 refineries. Their refinery in Mundra, Gujarat is one of the largest single-location refineries in India. As of September 30, 2021, they had 5,590 distributors located in 28 states and 8 union territories throughout India, catering to over 1.6 million retail outlets.

Promoters & Shareholding:

Adani Enterprises Limited, Adani Commodities LLP, and Lence Pte. Ltd are the company promoters.

| Pre Issue Share Holding | 100.00% |

| Post issue Share Holding | 87.92% |

Also read : Should Silver be a part of your investment portfolio?

Public Issue Details:

Offer for sale: Issue of approx. 156,521,739 equity shares of Rs. 1 aggregating up to Rs. 3600 Cr via book building route.

Total IPO Size: Rs. 3600 Cr.

Price band: Rs. 218 – Rs. 230.

Objective: To fund capital expenditure, repayment/prepayment of borrowings, and general corporate purposes.

Bid qty: minimum of 65 shares (1 lot) for Rs. 14,950 and maximum of 13 lots.

Offer period: 27th Jan 2022 – 31st Jan 2022.

Date of listing: 8th Feb 2022.

Pros:

· One of the few large FMCG food companies in India.

· Diversified product portfolio.

· Strong raw material sourcing capabilities.

· Professional and experienced management team.

· Extensive pan-India distribution network.

· Committed to maintaining environmental and social sustainability.

Cons:

· Since its products are in the nature of commodities, their prices are subject to fluctuations which might affect their profitability.

· COVID-19 pandemic has had and may continue to have certain adverse effects on its business.

· Subject to foreign exchange risks.

· Subject to business risks inherent to the palm oil and soy oil industries.

Subscribe or avoid?

Sectorial outlook – The Indian packaged food retail market, estimated at Rs. 6,00,000 Cr in FY 2020 contributes only 15% to the total food and grocery retail market estimated at Rs. 39,45,000 Cr in FY 2020. While the Indian food retail remains dominated by unbranded products such as fresh fruits and vegetables, loose staples, fresh un packaged dairy, and meat, the packaged food market is growing at almost double the pace of the overall category and is expected to gain a market share of 17% by FY 2025 and is expected to grow at an accelerated growth rate of approx. 14% till FY 2025. The shift towards packaged food from un packaged unbranded products, premiumization trend, and competition amongst bigger brands leading to innovative product offering is fuelling growth within packaged food and this is expected to have a positive impact on the Indian packaged food industry.

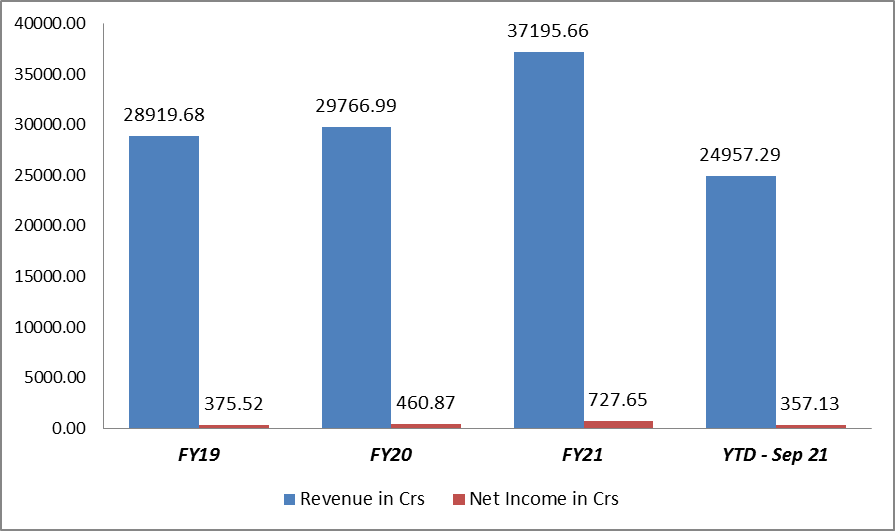

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 5 and the P/E is around 46x on the upper price band of Rs. 230. The EPS for FY21 is Rs. 6.37 and the P/E is around 36x. Hindustan Unilever (P/E 60), Britannia Industries (P/E 53.3), Tata Consumer Products (P/E 82.1), Dabur India (P/E 53.4), Marico Ltd. (P/E 50.5), and Nestle India (P/E 80.5) are its listed peers as per the RHP. The company P/E is between 46x and 36x, and looking at the industry average P/E, the listing seems to be reasonable.

Recommendation – It is one of the leading FMCG food companies in India and amongst the large FMCG players, a few players like Emami Agrotech, Patanjali, and Adani Wilmar have registered a double digit revenue growth rate in the last 5 years. Adani Wilmar has registered a high growth of 24% in its revenues in FY 2021 becoming among the top 5 fastest growing packaged food companies and it also has been able to keep up its profit margin. After considering all the factors we would recommend investors to “Subscribe” to this IPO in a medium to long term perspective.

Also read : Market Outlook for Jan’22

Disclaimer:

This article should not be construed as investment advise, please consult your Investment Adviser before making any sound investment decision. If you do not have one visit mymoneysage.in