AGS Transact Technologies Limited incorporated on December 11, 2002, is one of the largest integrated Omni-channel payment solutions providers in India in terms of providing digital and cash-based solutions to banks and corporate clients, as of March 31, 2021. The company is also the second-largest company in India in terms of revenue from ATM managed services under the outsourcing model, revenue from cash management and the number of ATMs replenished. It provides customized products and services comprising ATM and CRM outsourcing, cash management, and digital payment solutions including merchant solutions, transaction processing services, and mobile wallets.

Get your Free Wealth Management Tool, to explore your path to Financial Freedom now!

AGS Transact operates its business in the following segments: i) Payment Solutions; ii) Banking Automation Solutions; and iii) Other Automation Solutions (for customers in the retail, petroleum, and colour sectors). The company, as of August 31, 2021, has deployed 221,066 payment terminals and was one of the largest deployers of POS terminals at petroleum outlets in India, having rolled out IPS at 154 more than 16,000 petroleum outlets with 28,986 terminals. They have also expanded internationally to offer automation and payment solutions to banks and financial institutions in other Asian countries comprising Sri Lanka, Singapore, Cambodia, the Philippines, and Indonesia.

Promoters & Shareholding:

Satish Waman Wagh is the company promoter.

| Pre Issue Share Holding | 98.23% |

| Post Issue Share Holding | 66.07% |

Also read : All about investing in Infrastructure Investment Trusts (InvIT’s).

Public Issue Details:

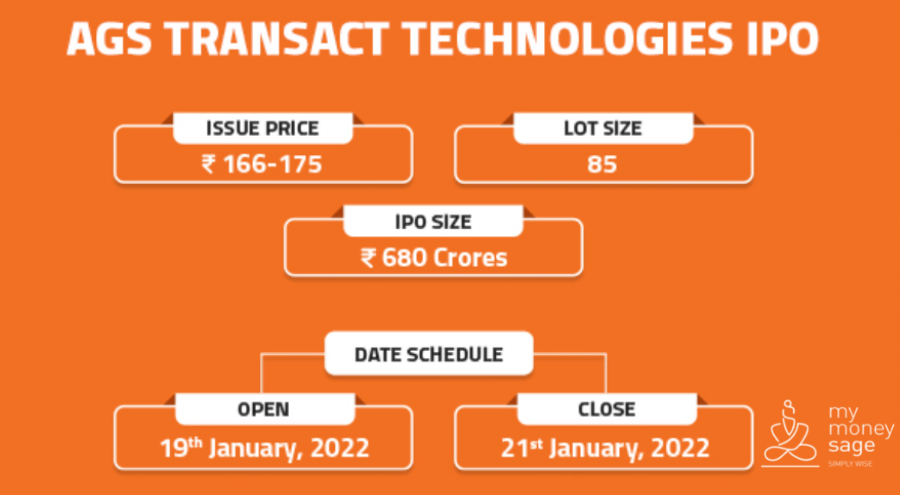

Offer for sale: OFS of approx. 18,248,175 equity shares of Rs. 10, aggregating up to Rs. 680 Cr.

Objective: To carry out an offer for sale by selling shareholders and to gain listing benefits of equity shares on the stock exchange.

Bid qty: minimum of 85 shares (1 lot) for Rs. 14,875 and maximum of 13 lots.

Date of listing: 1st Feb 2022.

Pros:

- One of the largest integrated Omni-channel payment solutions providers in India.

- Diversified product portfolio.

- Strong Capabilities to Develop Customized Solutions In-house.

- Professional and experienced management team.

- Dedicated In-house Infrastructure and Technological Capabilities.

Cons:

- A decrease in the use of cash as a mode of payment could hurt its business since it depends on the growth of the ATM network in India.

- COVID-19 pandemic has had and may continue to have certain adverse effects on its business.

- Any changes in interchange fees by the National Payments Corporation of India (NPCI), or through potential regulatory changes may harm its business.

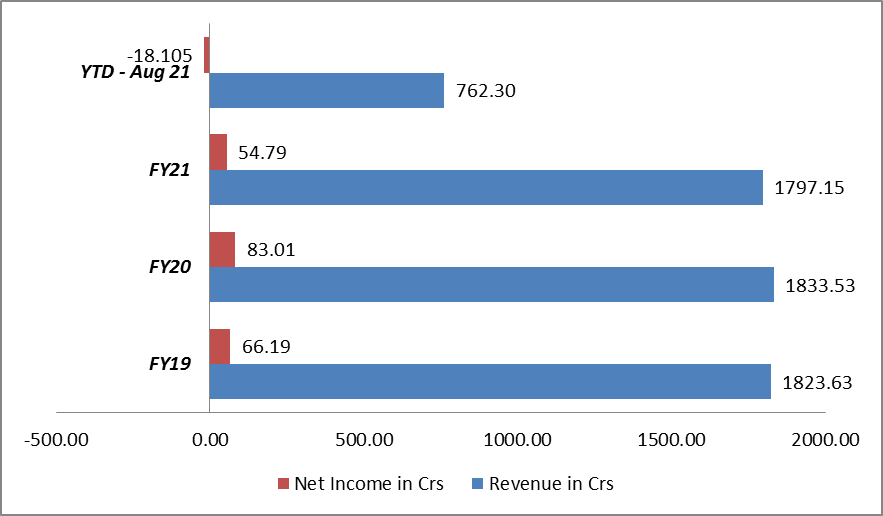

- Its revenue has been decreasing since the last 2 yrs.

Subscribe or avoid?

Sectorial outlook – Indian ATM management services market is at a developing stage. The ATM Managed Services Market is moderately fragmented among the top 6-7 players which constituted 60-70% of the revenue share though several smaller players are existing in the market. Indian government during August 2014 has initiated the scheme of opening up a bank account at zero balance under Pradhan Mantri Jan Dhan Yojana (PMJDY). This led to an expansion in the number of transactions performed in an ATM as debit card users in India increased significantly. The number of ATMs (excluding white label ATMs) installed increased from 199,099 as of March 31, 2016, to 213,575 as of March 31, 2021. The Indian ATM management services industry remains underpenetrated but it is expected to grow at a positive double-digit CAGR during FY21 to FY26 as the implementation of cassette swap takes place, this is expected to have a positive impact on the company and its business.

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 5.5 and the P/E is around 32x on the upper price band of Rs. 175. The EPS for FY21 is Rs. 4.55 and the P/E is around 38x. We cannot annualize the first 5 months ended at Aug-21 since the company has incurred losses. There are no listed peers as per the RHP. The company P/E is between 32x and 38x but we cannot determine whether it is under-priced or over-priced since it doesn’t have any listed peers.

Recommendation – Even though the company is one of the largest integrated Omni-channel payment solutions providers in India, it will be very difficult to grow the business because of the rise of digital payment services in recent years and the pandemic where even though ATMs and cash services were declared as essential services and remained functional, their AMC services, Banking Automation Solutions decreased by more than 20% and this pandemic might continue and may cause lockdown in certain areas which would adversely affect its business. After considering all the factors we would recommend investors to “AVOID” this IPO for now, investors with excess cash and high-risk profile can subscribe but risk-averse investors can just wait for the listing and they can get into it if they are able to identify some positive macro factors and the stock is trading at a discount.

Disclaimer:

This article should not be construed as investment advise, please consult your Investment Adviser before making any sound investment decision. If you do not have one visit mymoneysage.in

Also read : Market Outlook for Jan’22