Metro Brands Limited incorporated on January 19, 1977, is one of the largest Indian footwear speciality retailers and is among the aspirational Indian brands in the footwear category. The company caters to the footwear needs of customers through a wide range of branded products for the entire family including men, women, unisex and kids, and different occasions. The company retails footwear under its brands of Metro, Mochi, Walkway, Da Vinchi, and J. Fontini, as well as certain third-party brands such as Crocs, Skechers, Clarks, Florsheim, and Fitflop, which complement our in-house brands.

Get your Free Wealth Management Tool, to explore your path to Financial Freedom now!

As of September 30, 2021, Metro Brands operated 598 Stores across 136 cities spread across 30 states and union territories in India and they also operate 2 warehouses in India, both located at Bhiwandi in Maharashtra, on a leave-and-license basis. The company has been supported by Mr. Rakesh Jhunjhunwala as an investor since 2007.

Promoters & Shareholding:

Rafique A. Malik, Farah Malik Bhanji, Alisha Rafique Malik, Rafique Malik Family Trust and Aziza Malik Family Trust are the company promoters.

| Pre Issue Share Holding | 84.02% |

| Post Issue Share Holding | 74.27% |

Public Issue Details:

Offer for sale: Fresh issue of approx. 5,900,000 equity shares at Rs. 5, aggregating up to Rs. 295 Cr and OFS of approx. 21,450,100 equity shares, aggregating up to Rs. 1,072.51 Cr.

Total IPO Size: Rs. 1,367.51 Cr.

Price band: Rs. 485 – Rs. 500.

Objective: To finance the expenditure for opening new stores of the company and for general corporate purposes.

Bid qty: minimum of 30 shares (1 lot) for Rs. 15,000 and maximum of 13 lots.

Offer period: 10th Dec 2021 – 14th Dec 2021.

Date of listing: 22nd Dec 2021.

Also read : Market Outlook – Dec’21

Pros:

- One of the largest Indian footwear speciality retailers.

- Wide range of brands and products catering to all occasions across age groups and market segments.

- Professional and experienced management team.

- Asset light business with an efficient operating model.

- The company’s business is consumer-centric and they have loyalty programs for their customers.

Cons:

- Dependent on third parties for the manufacturing of all the products.

- Since both the company’s warehouses are located in the same region, any lockdowns will affect the company’s business.

- The company faces competition from existing footwear retailers, both organized and unorganized, and potential entrants to the footwear retail industry.

- The spread of the new covid variant might affect the company’s business.

Subscribe or avoid?

Sectorial outlook – The Indian footwear industry has witnessed an increase in activity over the last few years, with the changing consumer attitude towards footwear. Shoes, initially positioned as a value purchase, are now transcending into a lifestyle purchase. The demand for athleisure and sportswear is specifically expected to increase post the pandemic due to increased awareness about healthy living amongst the urban youth. The footwear segment comprises approximately 1.5% share of the total retail industry as of Fiscal 2020 and it is estimated at Rs. 1 trillion. The segment witnessed a decline of approximately 31% in Fiscal 2021 due to the lockdown restrictions imposed throughout the pandemic but going forward the segment to reach an estimated Rs. 1.4 trillion by Fiscal 2025, growing at a CAGR of approximately 21% between Fiscal 2021 and 2025.

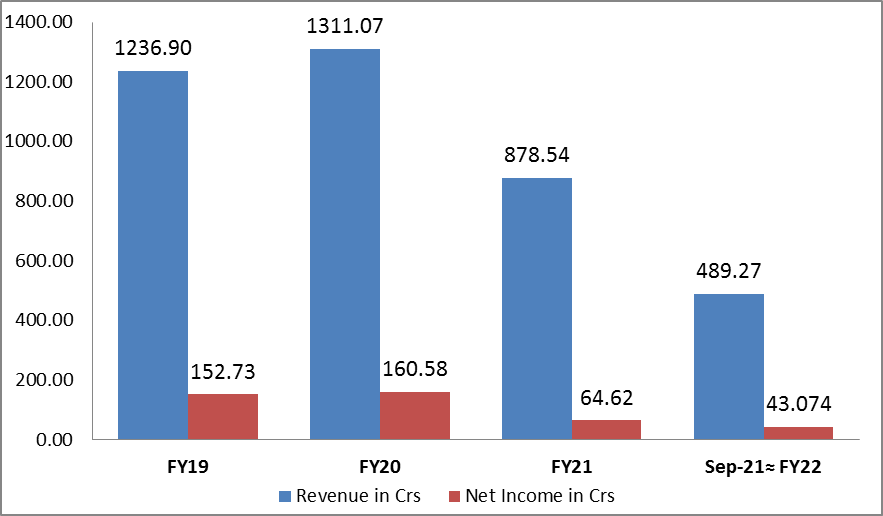

The financials (revenue and net profit) are shown in the graph below:

Valuation – For the last 3 years average EPS is Rs. 4.19 and the P/E is around 120x on the upper price band of Rs 500. The EPS for FY21 is Rs. 2.43 and the P/E is around 205x. If we look at the first 6 months ended at Sep-21 and annualize it to FY22 then the EPS is Rs. 1.62 and the P/E is around 154x. The listed peers of the company are Bata India and Relaxo Footwear (112x P/E). The company P/E is between 205x and 120x and after considering all the factors, the listing seems to be expensive.

Recommendation – The Company is one of the largest footwear brands in India but their revenue, as well as the profit margin, has been declining. Though the GMP of this IPO is hovering around 10%, we recommend investors to “AVOID” this IPO.

Also read : All you need to know about RBI’s Retail Direct Scheme

Disclaimer:

This article should not be construed as investment advise, please consult your Investment Adviser before making any sound investment decision. If you do not have one visit mymoneysage.in now.