Tega Industries Limited incorporated on May 15, 1976, is a leading manufacturer and distributor of specialized ‘critical to operate’ and recurring consumable products for the global mineral beneficiation, mining and bulk solids handling industry, on the basis of sales as of June 30, 2021. It is also the second largest producer of polymer-based mill liners, on the basis of revenues as of June 30, 2021. Tega offers comprehensive solutions to marquee global clients in the mineral beneficiation, mining and bulk solids handling industry, through their wide product portfolio.

Get your Free Wealth Management Tool, to explore your path to Financial Freedom now!

The company’s joint venture in India with U.K. branch of Hosch Group, Germany is engaged in precision conveyer belt cleaning and caters to various industries in India. They also have 18 global and 14 domestic sales offices located close to their key customers and mining sites. Tega has 6 manufacturing sites, including 3 in India, at Dahej in Gujarat and at Samali and Kalyani in West Bengal, and 3 sites in major mining hubs of Chile, South Africa and Australia, with a total built-up area of 74,255 Sq. mts.

Promoters & Shareholding:

Madan Mohan Mohanka, Manju Mohanka, Manish Mohanka, Mehul Mohanka and Nihal Fiscal Services Private Limited are the company promoters.

| Pre Issue Share Holding | 85.17% |

| Post Issue Share Holding | 79.17% |

Public Issue Details:

Offer for sale: OFS of approx. 13,669,478 equity shares of Rs. 10 aggregating up to Rs. 619.23 Cr.

Total IPO Size: Rs. 619.23 Cr.

Price band: Rs. 443 – Rs. 453.

Objective: To carry out OFS to provide exit opportunity and to achieve the benefits of listing the equity shares on the stock exchanges.

Bid qty: minimum of 33 shares (1 lot) for Rs. 14,949 and maximum of 13 lots.

Offer period: 1st Dec 2021 – 3rd Dec 2021.

Date of listing: 13th Dec 2021.

Pros:

- A leading producer of specialized and “critical to operate” products, with high barriers to replacement or substitution.

- Insulated from mining capex cycles, as the products cater to after-market spend, providing recurring Revenues.

- Professional and experienced management team.

- In-house R&D and manufacturing capabilities.

- Long standing market player with marquee global customer base and strong global manufacturing and sales capabilities.

Cons:

- Covid-19 pandemic might have adverse effect on its operation and supply chains.

- Dependent on a few key suppliers of certain raw materials and do not have long term contracts.

- Foreign exchange risks.

- Significant power, water and fuel requirements and any disruption in supplies could increase our production costs and adversely affect its operations.

Also read : All you need to know about Nippon India Taiwan Equity Fund

Subscribe or avoid?

Sectorial outlook – In 2020, Asia-Pacific accounted for 71% of the global mining industry, followed by North America with 9%. Global commodity mineral production during 2020 was 10.2 billion tons, with coal and Iron (2 largest minerals mined worldwide) accounting 96% of total production. Global crushing, screening, and mineral processing equipment market size was estimated at $20 billion in 2020. The market was growing at a CAGR of about 7% until 2019 but due to the COVID-19 pandemic, the overall demand declined in 2020. The industry is likely to recover in 2022 and is forecast to reach $36.9 billion by 2030, growing at a CAGR of 6.3%. The 2021 approval of the Mines and Minerals (Development and Regulation) Amendment Bill should help pave the way for increased domestic production and curtailed imports, increased private sector participation, and higher mining employment. This along with many other government plans is expected have positive impact on the company and its business.

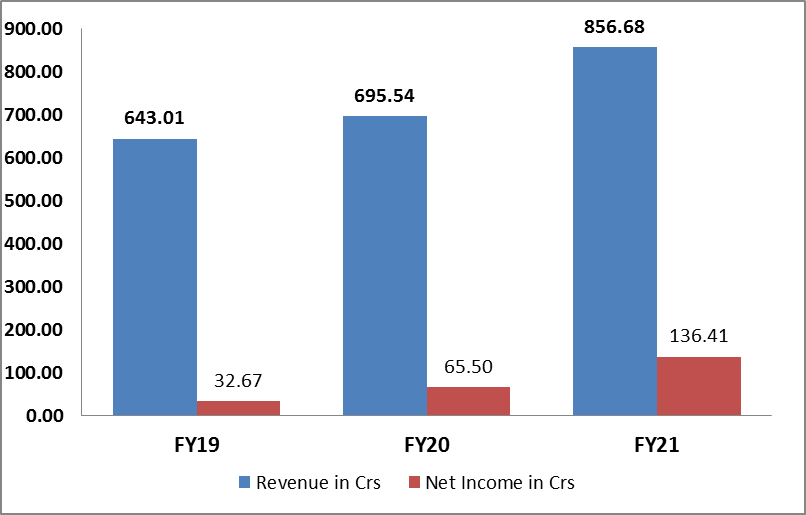

The financials (revenue and net profit) are shown in graph below:

Valuation – For the last 3 years average EPS is Rs. 14.34 and the P/E is around 31.5x on the upper price band of Rs 900. The EPS for FY21 is Rs. 20.48 and the P/E is around 22x. Its listed is AIA engineering limited (P/E 30.6x). Since the company P/E is is between 30.5x and 22x and after comparing it with its listed peers, the listing seems to be reasonably priced.

Recommendation – After considering all the factors we would recommend investors to “SUBSCRIBE” to this IPO for medium to long term perspective, with a possibility of both listing and long term gains.

Disclaimer:

This article should not be construed as investment advice, please consult your Investment Adviser before making any sound investment decision. If you do not have one visit mymoneysage.in now.

Also read : All you need to know about RBI’s Retail Direct Scheme